Are Employee Stock Purchase Plans Underrated?

Hello, I’m Kevin - a financial planner who helps tech professionals and their families live great lives.

Make yourself at home - we’ll get to whether ESPPs are underrated in a moment.

But first - here are some links you may want to save for later.

Own Stock or Contribute to ESPP?

Is It Worth Holding Employer Stock?

Now, let's get on to the blog! 😀

What Is an Employee Stock Purchase Plan?

An Employee Stock Purchase Plan is a way to potentially leverage employer stock with less risk.

Here's how the plan worked at a couple of my employers: each company offered a 15% discount and a six month lookback.

That meant the price I paid was 15% off the lower of the price at the beginning and end of six months.

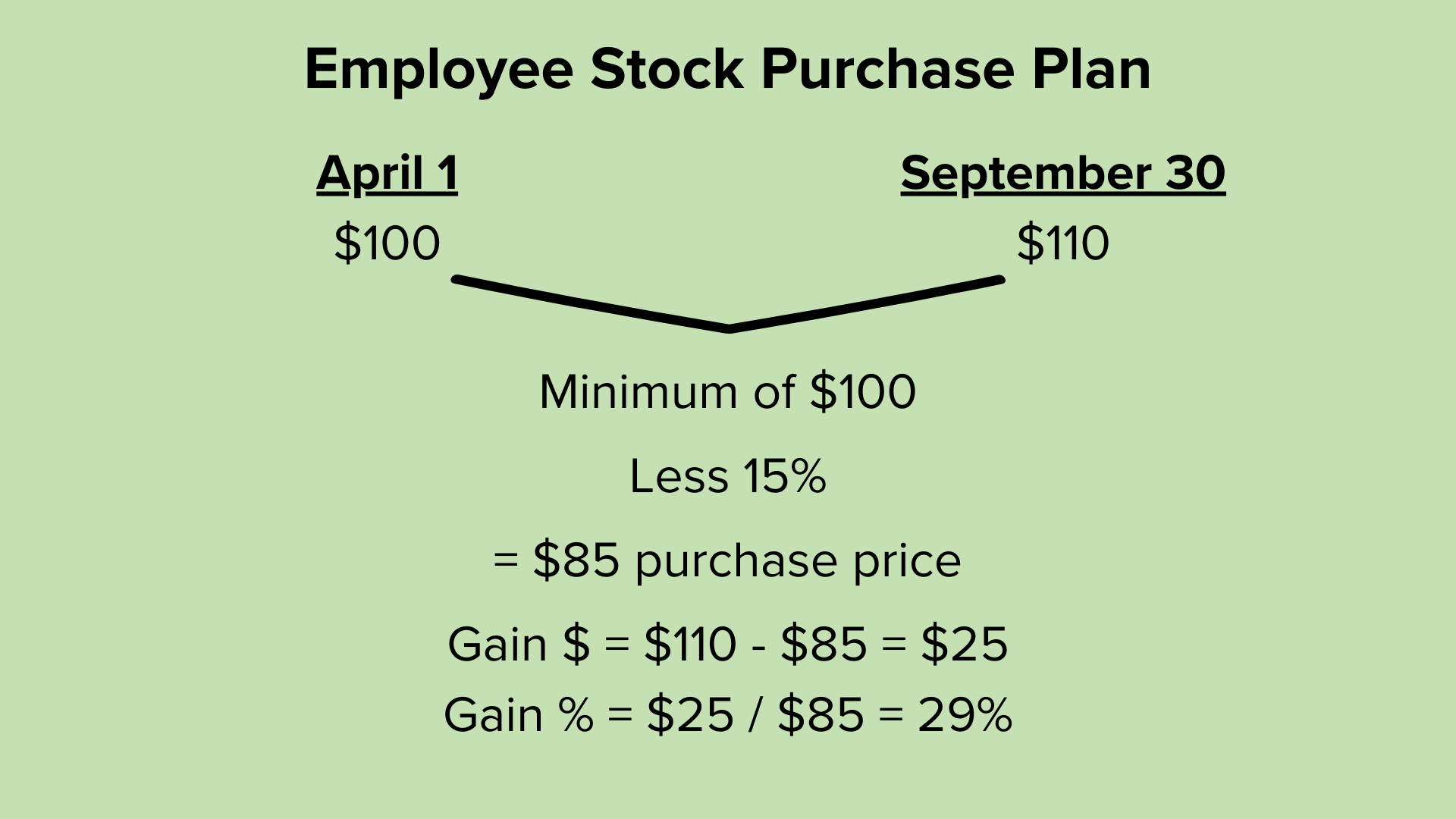

ESPP Example with a Rising Share Price

Let's say that on April 1st the stock price was $100.

It was a good six months! The stock rose to $110 by September 30th. The lookback took the lower of the two prices, so $100.

15% off that is an $85 purchase price.

Without trading restrictions, the shares can be sold immediately for $110. That's a $25 per share, or 29%, gain.

The employee may have hardly owned the stock! Remember, the underlying stock grew just 10% over the six months.

ESPP Example with a Flat Share Price

If instead the price had stayed at $100, the purchase price would still have been $85. However, the shares would only be worth $100.

That's a $15 (or 18%) gain for a very short time owned. Not bad, considering the underlying stock was flat for six months!

Mechanics of Purchasing Discounted Stock

To participate, someone would need to sign up at least a few weeks before the offering period begins.

They'd choose a percent of their income to contribute, up to 15%. For higher earners, there's also a contribution cap of $25,000 each year.

Once the six month offering period starts, after-tax dollars would drip into an account later used to buy shares at a discount on the purchase date. To fund the purchase plan, less cash would be deposited into the employee's checking account each payday.

Complexities

Employee Stock Purchase Plans don't all work the same.

Participating in a stock purchase plan isn't for everyone, especially those without the cash flow to swing it. Also, some employees may have trading restrictions which add risk to participating in the ESPP.

If someone can participate, selling soon after purchase might fund the next round of contributions.

Form 3922 to Report Taxes Correctly

Some of the most popular tax software programs default to give no credit for the after-tax dollars used to buy the shares. Without entering the information in correctly, they might treat the whole sale as taxable.

At the beginning of each year, participants receive a Form 3922 which can be used to fill out the tax forms correctly and avoid double taxation.

Be sure to keep these forms until after the shares are sold. That information will be used to file accurate tax returns.

Hey, thanks for learning more about Employee Stock Purchase Plans.

Just a reminder, I share a lot of resources that can help you.

Disclaimer

In addition to the usual disclaimers, neither this post nor this video includes any financial, tax, or legal advice.