Plan for Unexpected Expenses

Overview

Struggling to track every expense?

There’s another way!

This article explores:

which expenses get missed and

why including them matters.

We’ll review three overlooked expenses:

home repair & maintenance,

vehicle replacement, and

gifts & donations.

Finally, we’ll consider a top-down approach to catch hidden expenses.

Underestimates

Expenses are often missed when we estimate total spending.

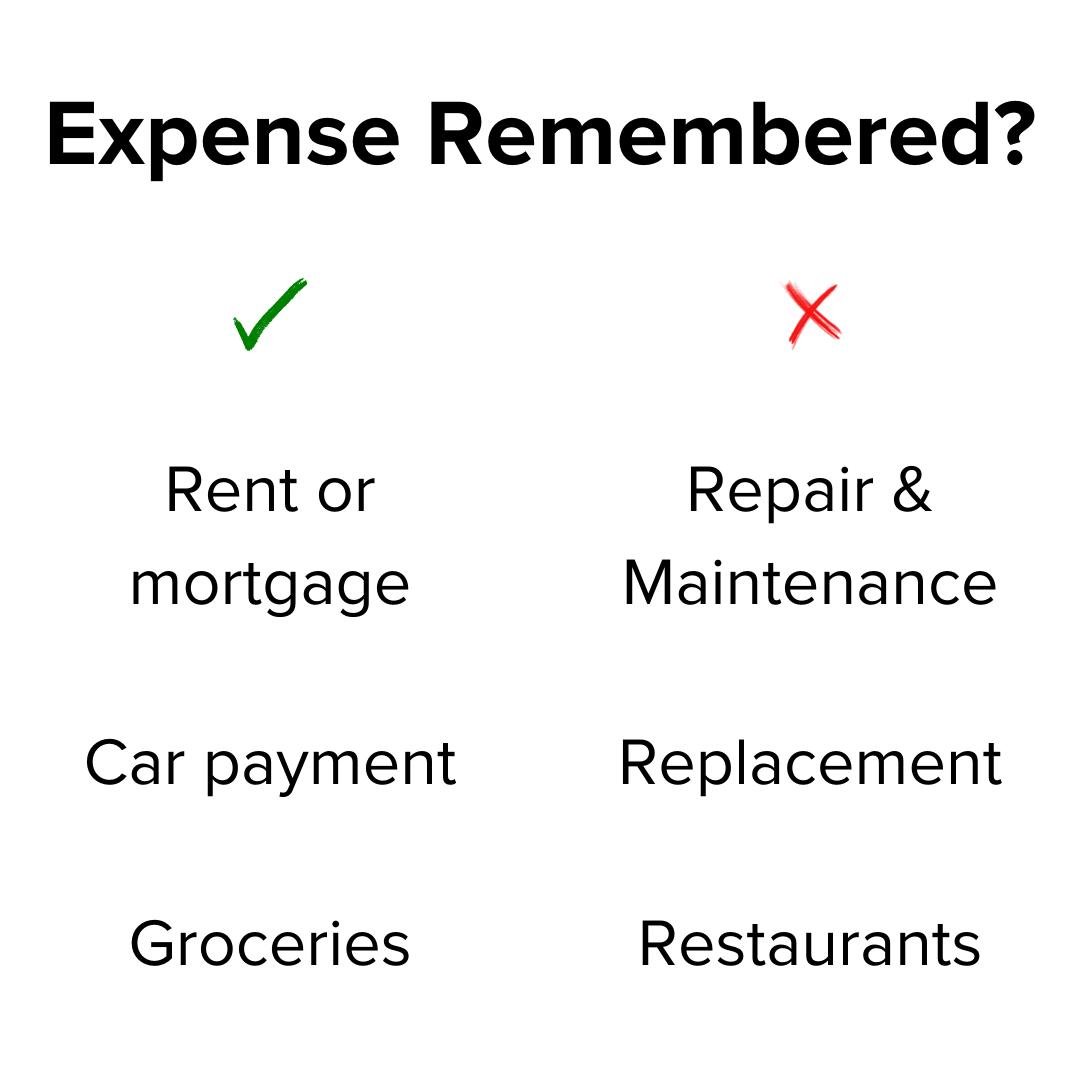

Remembered

We include regular expenses like:

rent or mortgage,

car payment, and

groceries.

Forgotten

However, we often forget the lumpy ones like:

repair & maintenance,

vehicle replacement, and

restaurants.

Why It Matters

Forgotten expenses can cause problems.

Frustration

Working hard only to have funds zapped by a surprise expense hurts.

It’s even worse when it impacts loved ones. A missed expense may force someone to break a promise.

Fees

Surprise expenses can also:

increase credit balances and interest charges,

generate late payment and overdraft fees, or

lower credit scores that raise interest rates.

These can create a vicious cycle.

Missed Benefits

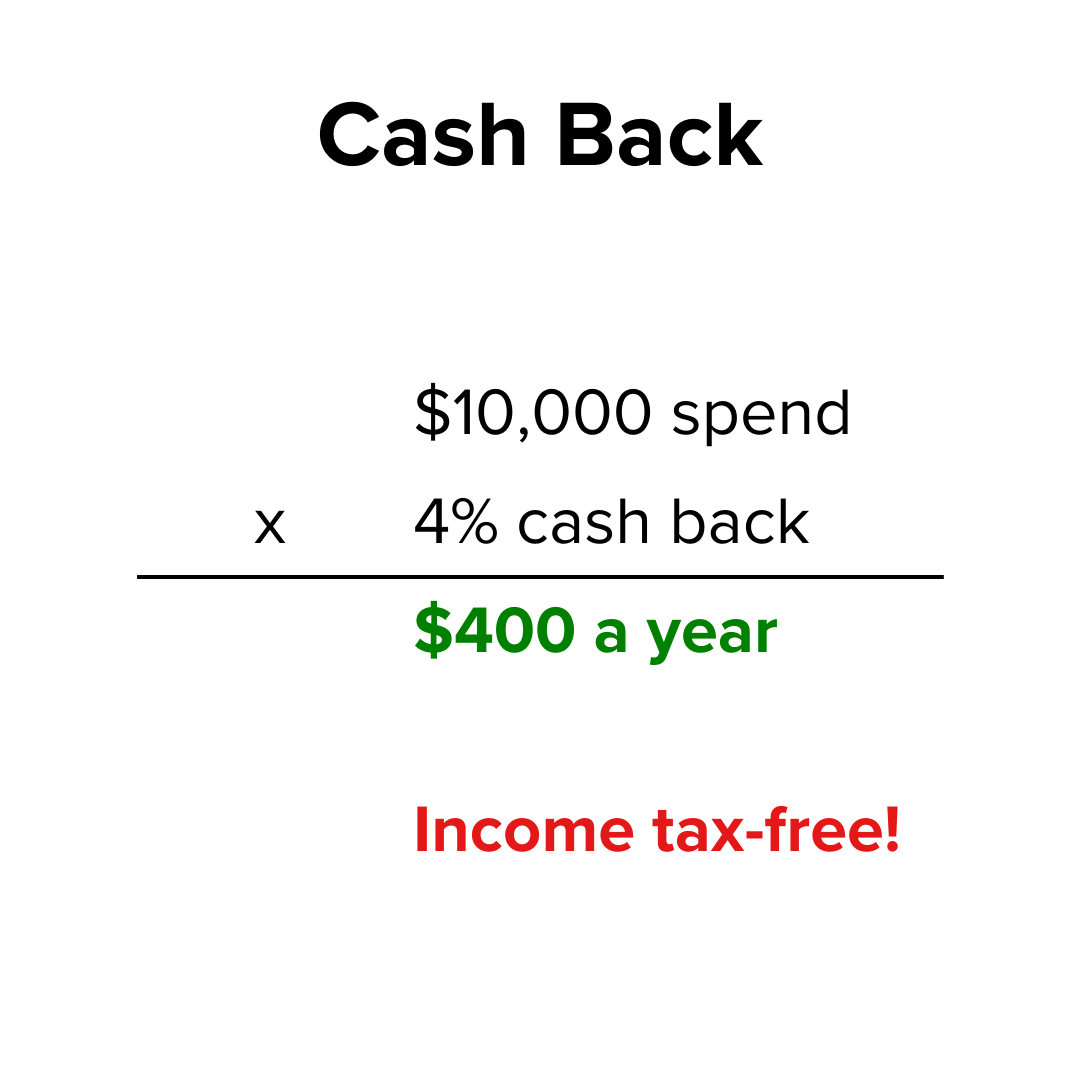

Overlooked expenses can also lead to missed opportunities.

Consider someone who doesn’t know they’re spending $10,000 a year at restaurants. They might not use a 4% cash back credit card.

They might miss out on $400 a year, tax-free!

Retirement Shortfall

The stakes are even higher when leaving the workforce.

What someone needs to save often depends on what they spend.

4% “Rule”

There’s something called the 4% “rule.” I consider it a rough guideline.

It suggests:

a $1 million portfolio

may support spending of $40,000 a year, plus inflation.

Of course, this isn’t a recommendation or advice. Retirement is too important to leave to guidelines.

Under-save

Some people use the inverse of the 4%. They multiply their spending by 25 to determine how much they need to save.

The calculation assumes their spending estimate is accurate!

Someone who misses $20,000 a year might retire with half a million ($500,000) less than they need!

1. Home Repair & Maintenance

Americans spend about half their budget on housing and transportation. Those are also the source of missed expenses.

Mortgage

We know our mortgage payment.

The amount often includes:

property taxes and

homeowners insurance.

Repair & Maintenance

However, the cost of upkeep is often missed.

We know something’s going to break - just not what or when:

roofs need to be replaced,

furnaces fail,

hot water heaters go out…

Experience

I have a long history with real estate.

Growing up, I helped my family build homes. We later bought and managed an apartment complex. Then, we bought properties during the Great Recession.

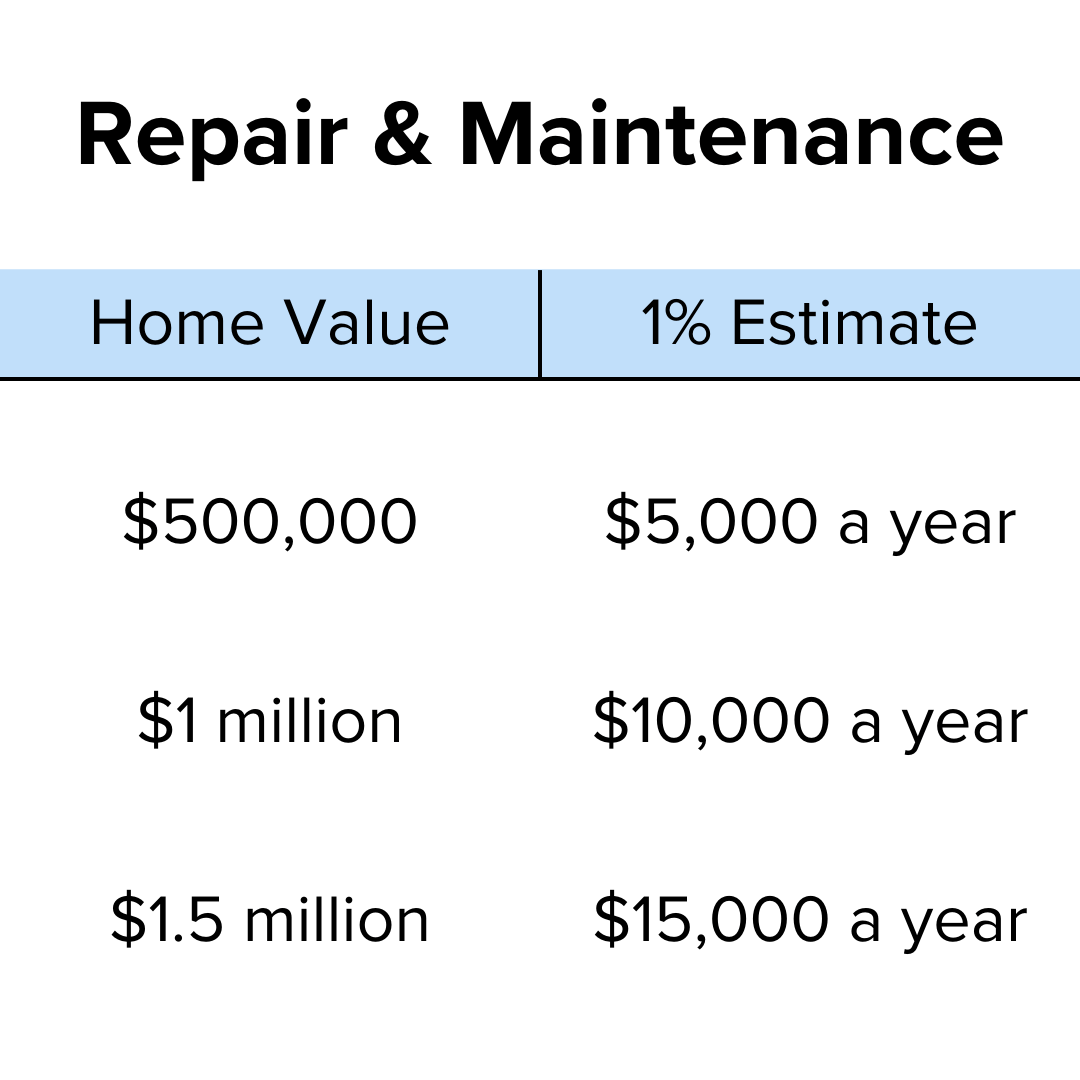

1% Estimate

I find 1% of a home’s value a decent estimate for annual repair and maintenance costs.

There are many nuances, including:

Homeowners Association (HOA) fees may be part of the cost.

Newer homes tend to need fewer repairs.

Major remodels, extensions, or additions are separate.

Homes on acres of land may cost less than 1% a year to maintain.

Examples

A $1 million home might cost $10,000 a year (1%) in repair & maintenance.

These expenses often grow with home value and inflation:

2. Vehicle Replacement

We remember our car payment.

What about when a vehicle is:

paid off or

bought with cash?

Funding

I ask people how they fund their vehicle purchases.

“We typically sell some stock” means it’s not in the regular budget!

Vehicle Purchases

People often include an estimate if they’re planning to buy a new car soon. However, that’s just one vehicle.

I ask how long they typically keep vehicles. 10 years is common.

A 40-year-old who plans to live to age 90 might buy five more vehicles!

If they only include the next purchase, their plan may miss four big-ticket purchases. Double that for two vehicles.

Annual Cost

Fortunately, estimating vehicle replacement isn’t hard.

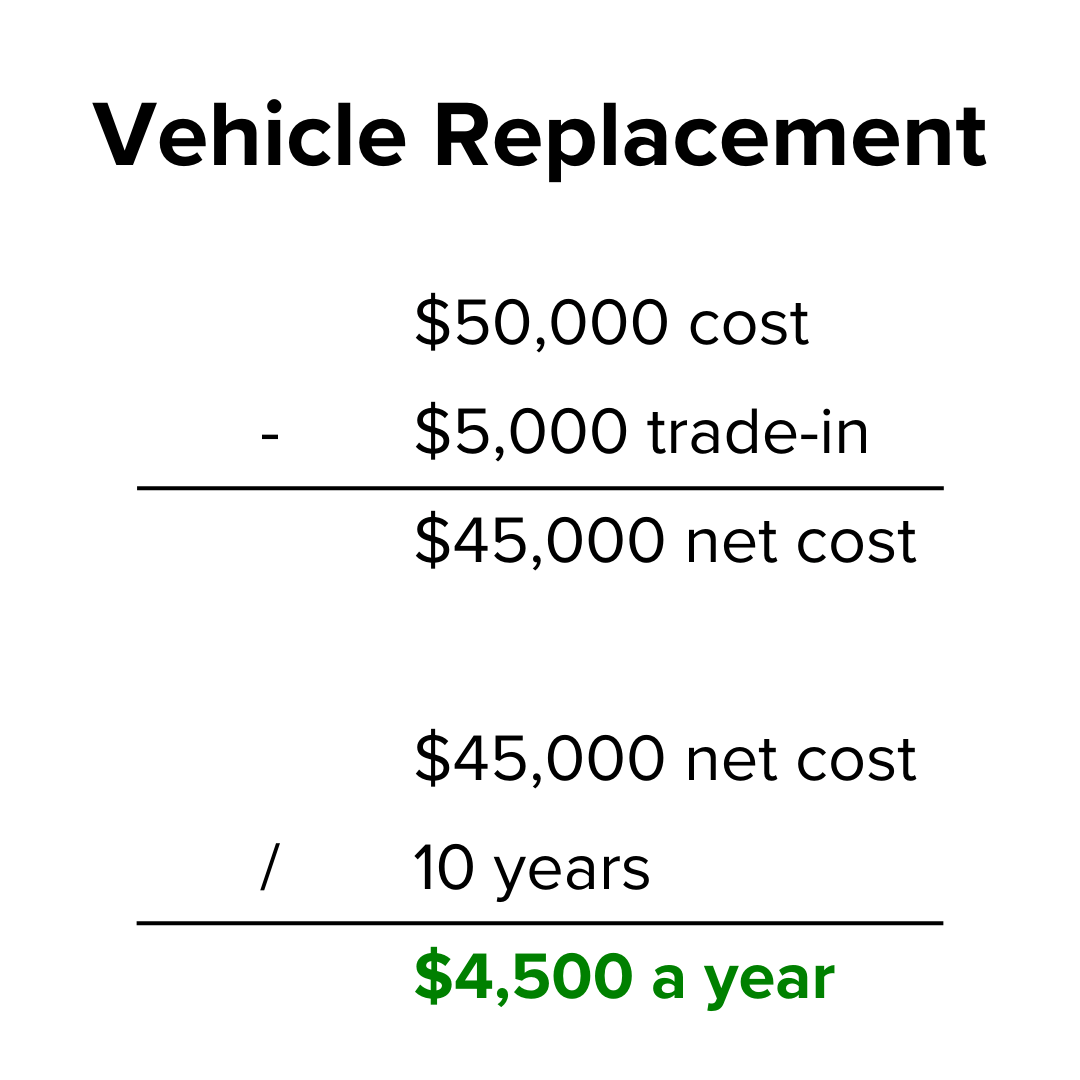

1. How long do you typically keep vehicles?

Let’s say 10 years.

2. How much might you spend on your next vehicle?

Let’s assume $50,000. Remember sales tax!

3. What do you typically get for your old vehicles?

That can depend on:

how much someone paid for the vehicle,

how long they kept it, and

how hard they were on it.

Consider trade-in, sale, gift, donation, and salvage value.

Let’s assume a $5,000 trade-in.

Calculation

Then, it’s simple math:

$50,000 purchase

less $5,000 trade-in

divided by 10 years

equals $4,500 a year.

I like to assume that cost:

for the rest of life,

growing with inflation.

It doesn’t really matter whether it’s financed or bought with cash.

I want people to have the option!

3. Gifts & Donations

Giving is another category that’s often overlooked.

Gifts

Gift expenses are often heaviest for:

education,

holidays, and

birthdays.

However, don’t forget:

weddings,

anniversaries,

Valentine’s Day,

Mother’s Day, and

Father’s Day.

Donations

Charitable contributions are planning opportunities.

Cash

While it certainly depends on the situation, cash may not be efficient.

“Friends don’t let friends give cash.” 😆

Still, cash may work best in some situations - especially if donations are matched by an employer.

Other Giving Options

Tax-advantaged donations include:

appreciated assets,

Donor-Advised Funds (DAFs),

Qualified Charitable Distributions (QCDs),

and more.

Forecast

More important than how donations are given is whether they’re included in the forecast.

I like to estimate annual giving, and grow it for inflation.

However, opportunities can arise as we age - especially if someone would owe state or federal taxes.

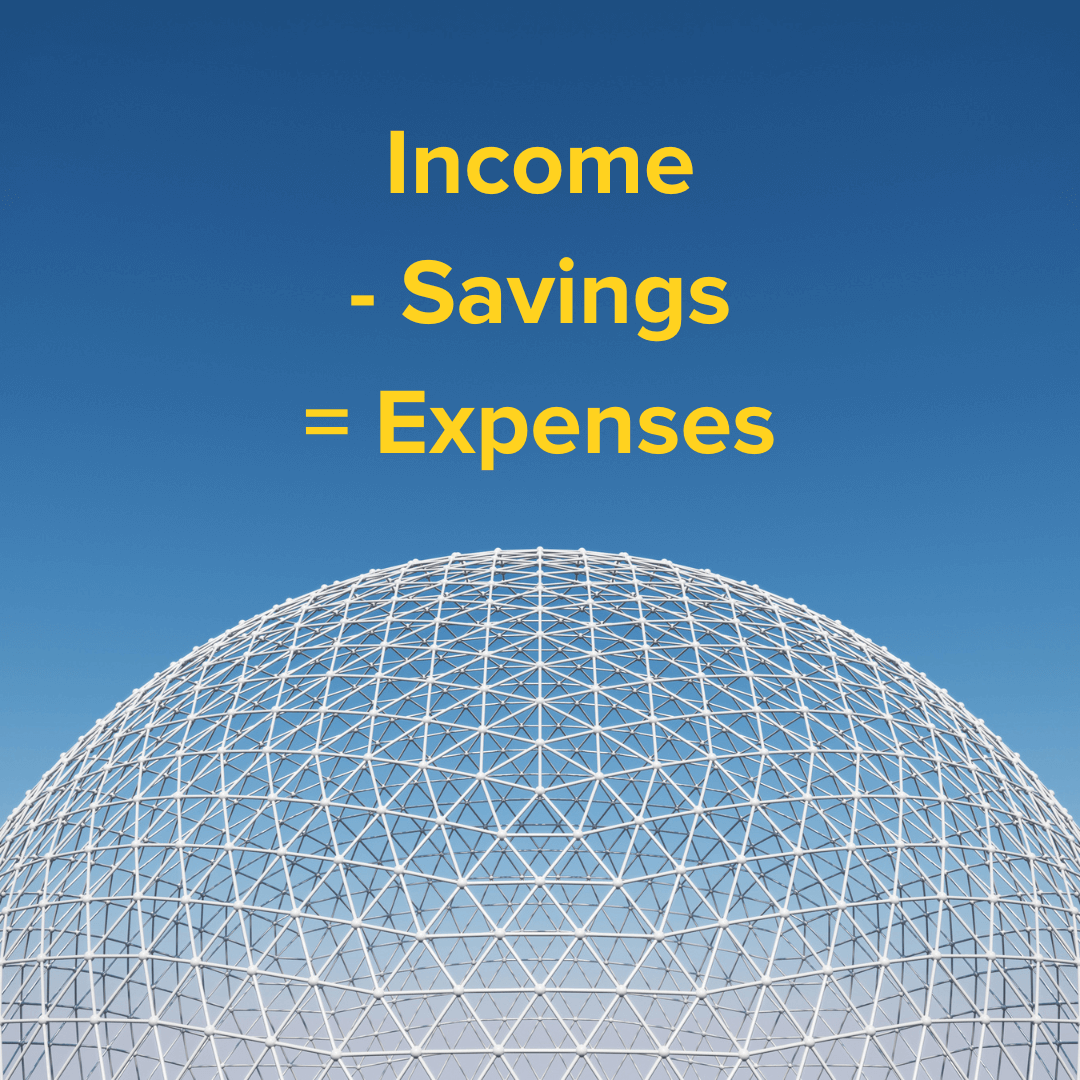

Top-Down Approach

It’s nearly impossible to remember every expense.

Fortunately, there’s a simple way to estimate total spending.

Expense Equation

It’s often easier to estimate:

income and

saving for a year.

Cash flow is a closed system! If income isn’t saved, it’s usually spent.

Income

I like to focus on total income and major expenses.

Tax returns and W-2’s are especially helpful for income.

Expense Buckets

A total is tough to digest. I review major categories.

Required

Major expenses can include:

state and federal income taxes,

Social Security and Medicare taxes,

mortgage principal and interest,

property taxes,

home repair and maintenance,

car payment or vehicle replacement,

life, disability, home, auto, and umbrella insurance,

healthcare premiums, and

utilities.

Discretionary

Some categories are more difficult to estimate:

groceries,

restaurants,

clothing,

gas,

entertainment,

travel,

gifts, and

donations.

Expense tracking is especially helpful for these variable costs.

The top-down approach sizes the total without knowing every detail.

Conclusion

It’s important to know your overall spending.

However, you don’t need to track every expense! Income minus saving is a spending estimate.

Be sure to include enough for home repair & maintenance, vehicles, and giving to fund your lifestyle!

Hey, thanks for reading my article on unexpected expenses!

Just a reminder, I share resources that can help you.

Join the newsletter and get the white paper:

Personal Finance for Tech Professionals

Disclaimer

In addition to the usual disclaimers, neither this post nor these images include any financial, tax, or legal advice.