Potential Financial Steps for Tech Professionals in February 2026

Wonderful time of the year

Forget December. Now is the most wonderful time of the year for many tech professionals!

That’s when you may:

get a raise,

receive an annual bonus, and

vest Restricted Stock Units (RSUs).

Potential steps this month

Financial steps could include:

update saving,

schedule tax prep meeting,

gather tax forms,

accept RSU grant, and

rebalance portfolio.

1. Update saving

The T-Mobile annual raise and bonus are typically communicated around Valentine’s Day. I always loved getting the good news and celebrating with my wife!

However, it sounds like it might be a bit later this year.

Raise

The annual merit increase is often a whole percentage.

Keeping up with inflation?

It’s important to consider whether a raise beats inflation.

The 12-month percentage change in the Consumer Price Index (CPI) ending December 2025 was 2.7%.

If your raise is below 3%, it may be because you:

recently received an increase,

accepted a promotion, or

are at the top of your pay band.

It might also be a sign of trouble in your current position.

Nonetheless, raises help employees automatically save more.

Same contribution rate

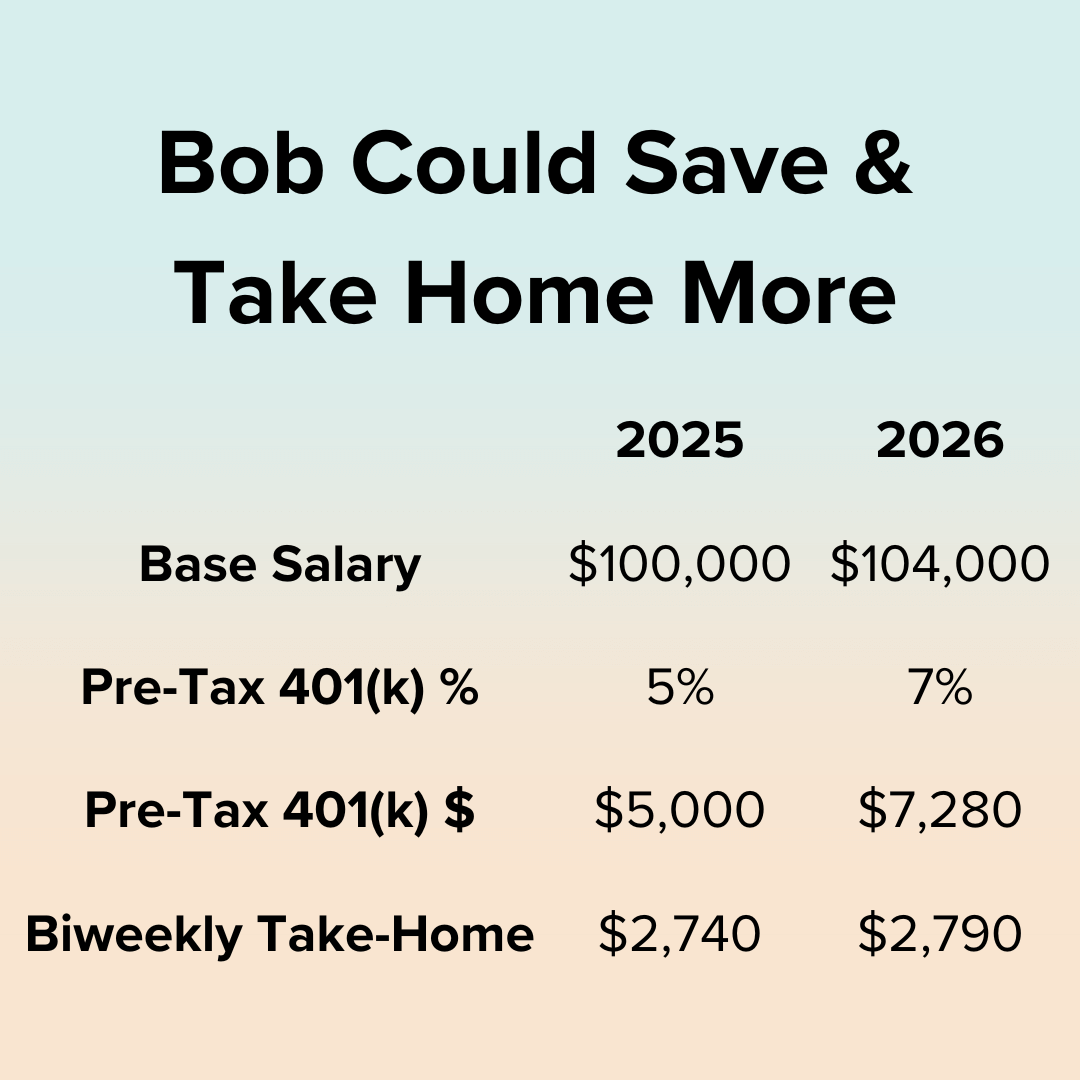

Let’s say Bob was earning $100,000 and got a 4% raise. He now earns $104,000 in base salary. Congratulations!

Bob contributes 5% of his gross income to his pre-tax 401(k) to get the full company match.

Without any other changes, his pre-tax 401(k) contributions would rise $360 for the year.

Bob contributes $200 more:

from $5,000 (5% of $100,000)

to $5,200 (5% of $104,000).

The company matches $160 more:

from $4,000 (4% of $100,000)

to $4,160 (4% of $104,000).

Gain without pain

However, raises are a great time to save more without feeling it.

Let’s say Bob bumped his pre-tax 401(k) contribution rate from 5% to 7%.

His 401(k) contribution rises $2,440 for the year!

Bob contributes $2,280 more:

from $5,000 (5% of $100,000)

to $7,280 (7% of $104,000)

… in addition to the $160 more from the company.

The best thing is that Bob’s take-home pay might still rise! It could grow from $2,740 to $2,790 per paycheck. That’s nearly $1,300 more a year!

Receiving more while saving more is a win!

This trick comes courtesy of my grandmother. She consistently saved half of her and my grandfather’s raises.

Bonus

Tech bonuses are no joke.

At T-Mobile, salaried employees are on the Short-Term Incentive Plan (STIP). The annual bonus has both an individual and company component.

The split varies by pay level. The theory is that the higher up someone is, the more impact they have on the whole company.

Individual

The individual portion is based on the employee’s performance according to their leaders:

above 100% is good;

below… not so much.

Individual payouts were about 100% for years. However, variation was added to reward extra effort.

Company

The company portion is tied to overall performance. It’s based on a set of targets.

In good years, it can be well over 100%.

Uncertain

My wife and I never took my annual bonus for granted. We knew the company might pay a low one - or none at all.

Bonus paychecks are mixed:

good - they provide significant income;

bad - they can be heavily taxed.

Retirement saving options

A company may offer:

pre-tax 401(k),

Roth 401(k), and

after-tax 401(k).

There’s also a spousal IRA option outside of the employer.

Pre-tax 401(k)

Saving some of the bonus to a pre-tax 401(k) has three primary benefits:

reduces taxable income (and likely income tax),

gives investments more time to grow, and

reduces how much needs to be taken out of the biweekly paychecks to reach the contribution limit.

The 2026 employee 401(k) contribution limits are:

$24,500 for those less than 50 years old,

$32,500 for those aged 50-59 as well as 64+, and

$35,750 for those aged 60-63.

There’s now a higher catch-up limit for workers aged 60-63. It’s $11,250 instead of $8,000 for other savers who are 50 years old and wiser.

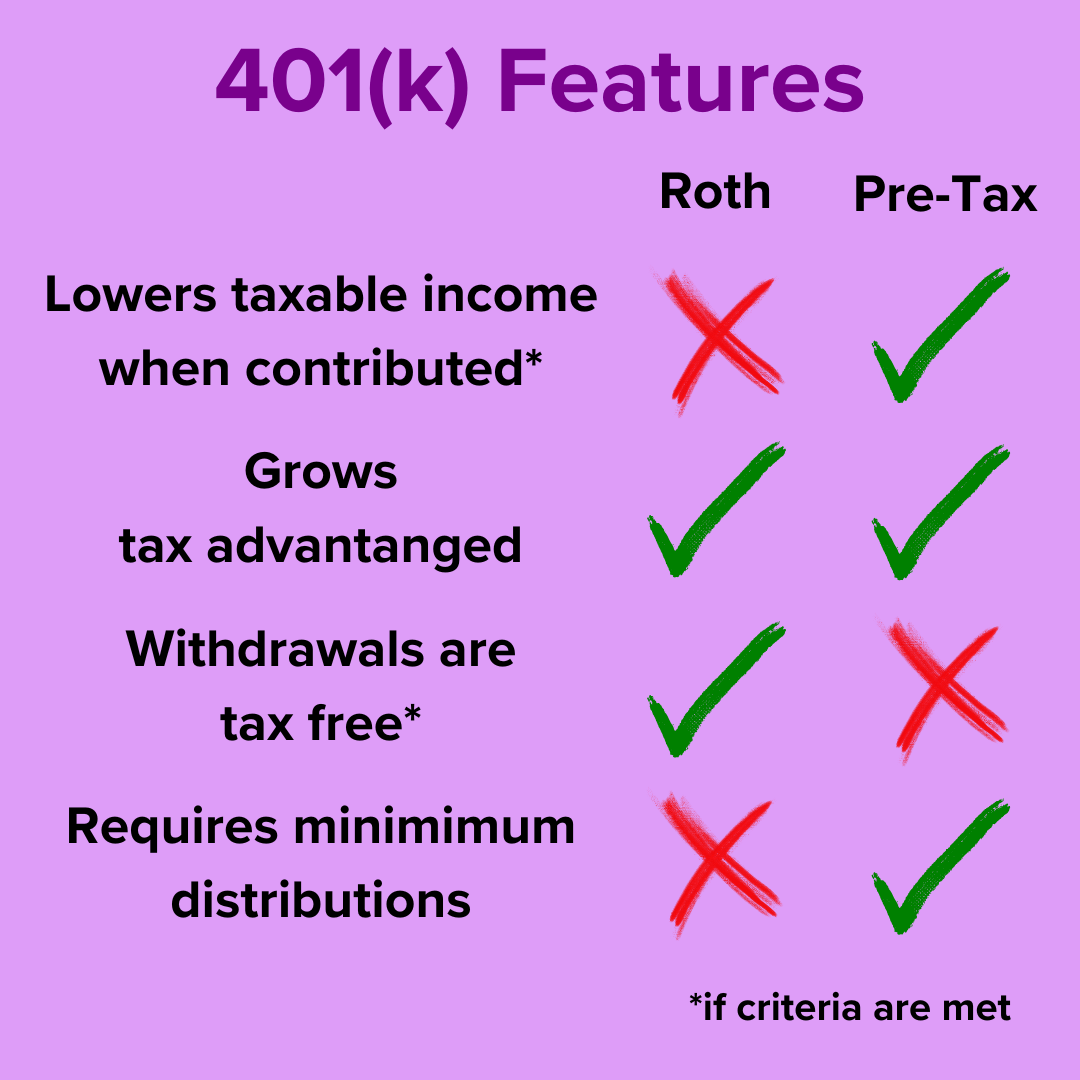

Roth 401(k)

Another option is the Roth 401(k), sometimes shortened to Roth(k).

The Roth benefit is that someone pays income taxes now and - if certain criteria are met - never pays income tax on the funds again!

The Roth option might appeal to someone if they:

don’t need the money for living expenses or debt payments,

anticipate their income will grow significantly in the future,

expect to continue to work until full retirement age, and/or

might move to a state with a higher income tax rate.

Here’s a quick comparison of the Roth and pre-tax 401(k) features:

After-tax

Many tech companies added the after-tax option more recently.

This plan is especially helpful for higher income employees looking to save on top of pre-tax contributions like their:

401(k) and

Health Savings Account (HSA).

The regular 2026 contribution limits are:

$24,500 for employee pre-tax/Roth 401(k) contributions and

$72,000 in total defined contributions.

The company match also counts toward the $72,000 limit.

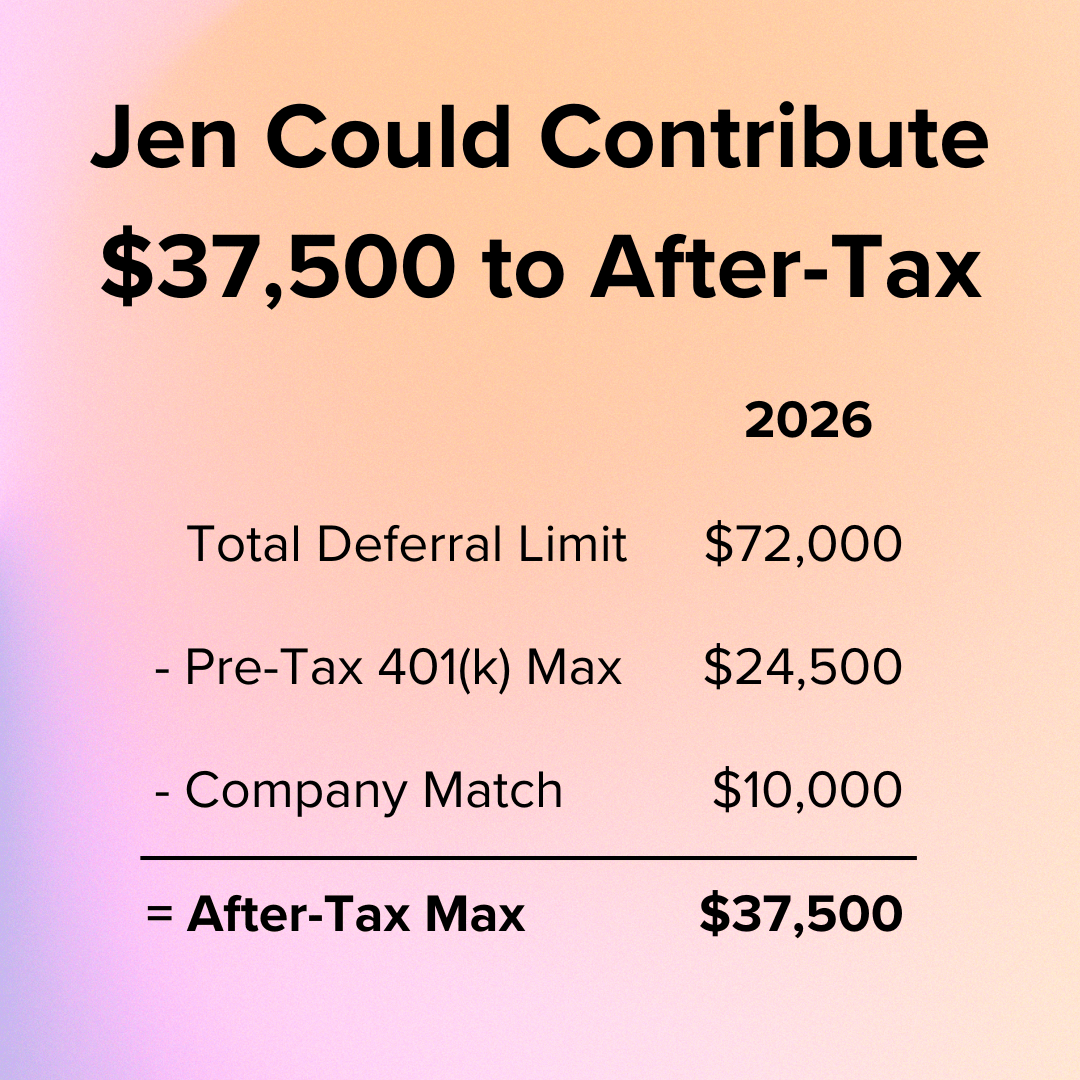

After-tax example:

Jen is a 45 year-old who earns a $200,000 salary and a $50,000 annual bonus. Congratulations!

Jen maxes her pre-tax 401(k) contributions at $24,500. Her employer also matches $10,000 (4% of $250,000).

That leaves $37,500 for her to contribute to the after-tax account:

$72,000 total defined contributions limit

less the $24,500 employee contribution

less the $10,000 company match.

Some plans allow money to move out of an after-tax account while the employee is still employed. That’s called an in-service distribution. Jen may be able to sweep funds directly into a Roth 401(k) or Roth IRA.

That’s important because gains in an after-tax 401(k) are taxed when withdrawn. Later distributions from a Roth 401(k) or Roth IRA typically aren’t.

It may be easier to roll funds into the Roth 401(k). Jen may even be able to get her custodian (such as Fidelity) to transfer her after-tax 401(k) contributions to a Roth 401(k) automatically.

The fancy term for this process is Mega Roth or Mega Backdoor Roth.

Spousal IRA

A fourth retirement plan is separate from the employer.

A spousal Individual Retirement Arrangement (IRA) is an account a spouse can contribute to despite earning little or no income.

If the couple is married and files a joint tax return, they may be able to:

stash some cash into the spouse’s account,

reduce their tax bill, and

invest for long-term growth.

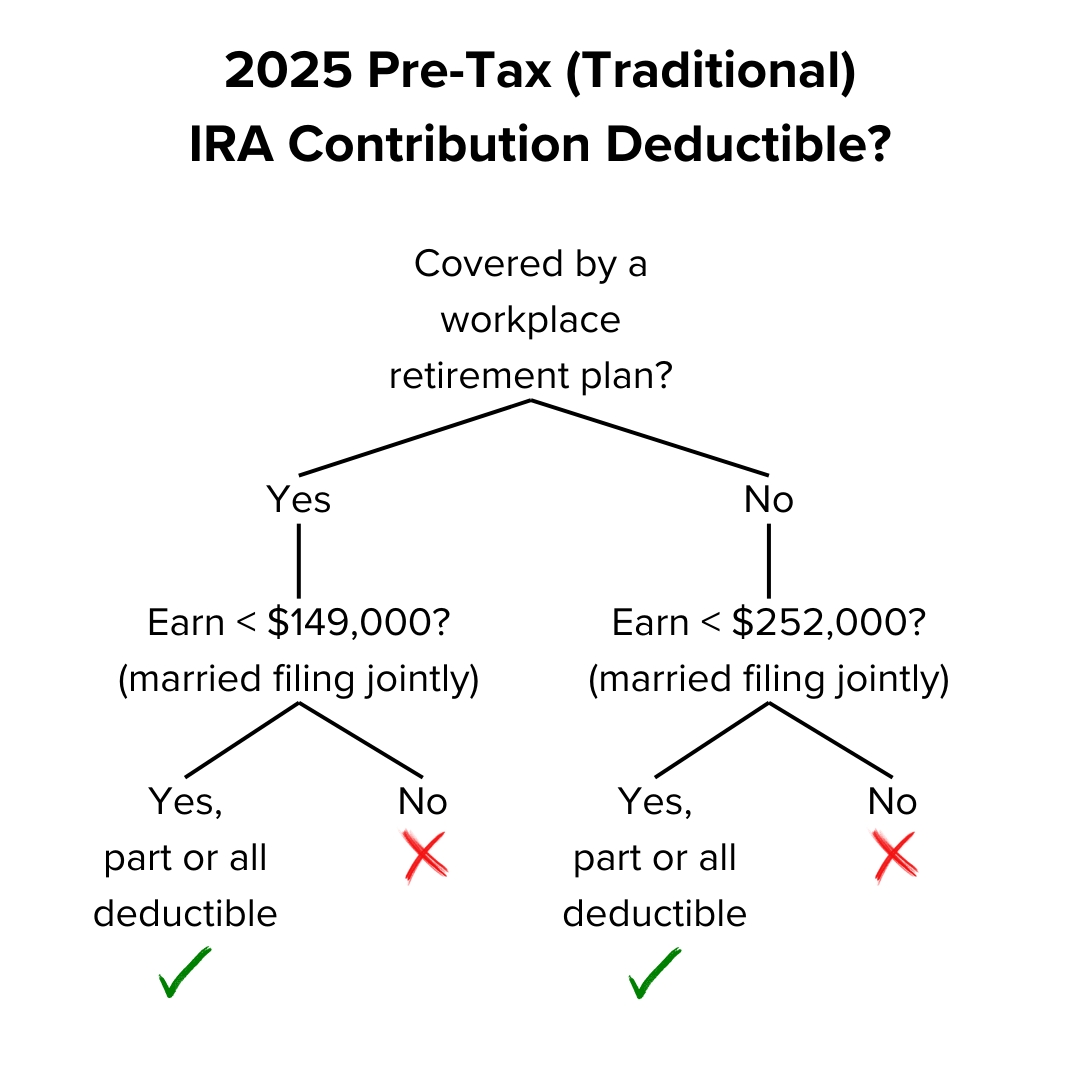

Here’s the best part: a 2025 contribution can be made until 4/15/2026! The February bonus may be perfect for a last-minute spousal IRA contribution.

Whether the contribution would lower taxable income depends on:

whether the spouse was covered by a retirement plan at work and

how much the couple earned in 2025.

Below is a quick decision tree based on whether the spouse is or is not covered by a workplace retirement plan.

For more tax saving ideas, check out 5 Ways to Lower Taxes Besides Donations. Whether to contribute to pre-tax, after-tax, or both depends on someone’s situation and goals.

Yikes - that was a lot about raises and bonuses!

However, it’s so important that it deserved some extra love. ❤️

2. Schedule tax prep meeting

Another step tech professionals and their families might take now is to schedule their tax prep conversation.

Even if you prepare your own taxes, it’s important to devote time to them.

Scheduling time is even more important when working with a tax preparer! They’re generally overworked and in high demand.

Get organized and come prepared!

3. Gather tax forms

One way to get organized is to create both a physical and digital folder for 2025 tax documents.

Physical folder

All tax documents received in the mail would ideally go into the tax folder.

W-2: salaries, wages, and taxes withheld;

Form 1095: health insurance coverage details;

Form 1098: mortgage repayment, interest, and property taxes;

Form 1099: many uses;

Form 3922: details on stock purchased through a qualifying plan like an Employee Stock Purchase Plan (ESPP); and

Schedule K-1: income, losses, and dividends for partnerships, S corporations, trusts, and estates.

Some of the most common Form 1099 types are:

NEC: Nonemployee Compensation (freelance income);

B: gain or loss on stock;

INT: interest;

DIV: dividends;

R: retirement plans;

T: tuition payments;

MISC: miscellaneous, etc.

A custodian (Fidelity, Vanguard, Schwab…) may include several forms in one file.

Digital folder

It’s best to save digital versions of all tax documents.

Two options include:

downloading directly from financial institutions and

scanning a copy of forms received in the mail.

Even if I receive a physical copy, I like to download the forms. It’s a way for me to double-check I don’t miss anything and that I’m using the latest version.

Places to download forms include:

banks and credit unions for interest paid or received,

custodians for investments, and

employer portals for W-2 compensation detail.

Since personal credit card interest usually isn’t deductible, those statements rarely need to be downloaded.

However, it’s a good idea to check every other financial account for important tax documents. Streamlining the number of accounts reduces workload - especially during tax season!

Tax checklist

Everyone’s busy. Things get missed - even by tax preparers!

Checklists save

Crashes happened frequently in the early days of aviation. Adding checklists significantly improved safety.

Checklists have spread to other areas like:

building construction,

truck driving, and

surgery.

We even use checklists when preparing to sail!

Tax checklist example:

One thing I like to do both for myself and for clients is draft a tax checklist. It lists everything I think could impact taxes for the year!

A good place to start is the previous year’s tax documents:

Which still apply?

Did anything change?

Creating the checklist reminds me of other things!

My personal checklist is in Microsoft Excel and I:

start with last year’s list,

remove what’s no longer relevant, and

add new items.

As I work through the list, I cross them off and record the date accomplished.

Once all the actions are complete, I carefully review our tax return inputs with my wife. Explaining the taxes helps clarify our thinking! She asks wonderful questions and checks other tax-impacting items.

Measure twice, cut once.

4. Accept RSU grant

It typically makes sense to accept RSU grants once they’re available.

Restricted Stock Unit grant

Even if someone is certain they’re going to leave their employer, it still makes sense to accept grants!

Some situations might result in a partial or complete vest:

new manager, team, department, or role,

layoff,

merger or acquisition,

employee death…

Accepting the grant early ensures it isn’t forgotten.

Restricted Stock Unit vest

RSU vesting depends on the company.

Two years ago, T-Mobile started issuing grants which vest every six months instead of once a year. For employees with grants from multiple years, they’ll likely still receive more shares around February 25th. However, they’ll probably also receive a sizable vest around August 25th. It may take a business day or two for shares to settle into employee accounts.

For most employees, some units are automatically sold to cover taxes. Employers provide the custodian with a tax percentage estimate. The custodian (such as Fidelity) then sells shares and sends the proceeds to the IRS and state governments for income taxes.

There’s good, bad, and great news for employees:

good - may not have to manually pay the RSU taxes;

bad - receive fewer shares of company stock; and

great - may be able to sell shares without paying additional tax.

Choosing to keep the shares is like an employee taking cash out of their checking account to buy more company stock.

Is that what they want to do? 🤔

5. Rebalance portfolio

After a bonus or Restricted Stock Units (RSUs) vest is a great time to review and potentially rebalance your investments.

It’s often important to have at least three to six (3-6) months’ of living expenses in a cash reserve.

Asset allocation

Next, check that the investment categories are close to the target percentages. Market performance and recent saving may have thrown off the allocation.

For example, tech stocks have had a wonderful run recently. You may have too much riding on this one industry!

Asset location

Is each of your investments held in the right account?

If either the asset allocation or location is off, it likely makes sense to adjust. However, consider the tax impact.

Thanks for reading my post on potential financial steps for tech employees in February. Happy Valentine’s Day! 💝

Just a reminder, I share many resources that can help you.

Sign up to get the white paper:

Personal Finance for Tech Professionals

Disclaimer

In addition to the usual disclaimers, neither this post nor this image includes any financial, tax, or legal advice.